A quarter that seems unusually calm and suspiciously orderly.

Lyst has just published its report for Q4 2025, and the results are somewhat unusual. The top three brands—Saint Laurent, Miu Miu, and COS—remain unchanged from the previous quarter, and if we look at the same period last year, the houses led by Anthony Vaccarello and Miuccia Prada have simply swapped places, returning to a hierarchy that is all too familiar for a year that promised so much creative movement.

Over the last twelve months, the industry has experienced a frenetic ‘game of musical chairs’ in which creative directors have come and gone, accompanied by new narratives and new beginnings. Everything pointed to disruption, radical changes and total restarts. However, the ranking suggests another, much more interesting interpretation, which is that perhaps the real breakthrough lies in not feeling the need to change everything.

Stability at the top does not imply immobility. The brands that are gaining ground today are not chasing spectacle or forced novelty. They are doing something quieter and, at the same time, more strategic: reinforcing codes, refining silhouettes and relying on what already works. In a year that was supposed to be marked by change, the winners have opted for consistency.

COS maintains its third position and records a 60% quarter-on-quarter growth in demand on Lyst. Its refined aesthetic, focus on materials and product consistency continue to connect with a global audience seeking quiet luxury. Massimo Dutti‘s entry in sixteenth place also points in the same direction: consumers are rewarding brands that are perceived as accessible, reliable and design-conscious, far removed from constant dependence on seasonal trends.

One of the biggest movements of the quarter was led by Ralph Lauren, which rose five positions with a 24% increase in demand compared to the previous period. Its momentum comes from its visual narrative and the lifestyle it proposes. In December, the Ralph Lauren Christmas aesthetic went viral on social media, generating 16,800 posts with the hashtag #ralphlaurenchristmas and 33,300 with #ralphlaurenaesthetic on Instagram and TikTok.

Burberry and Gucci, both climbing five places, and Stone Island, rising four places with a 62% increase in searches, demonstrate the same pattern: brands that actively reaffirm their identity—whether through historical codes, a disciplined design language, or a clear cultural alignment—are gaining relevance in a market that is beginning to value consistency over reinvention.

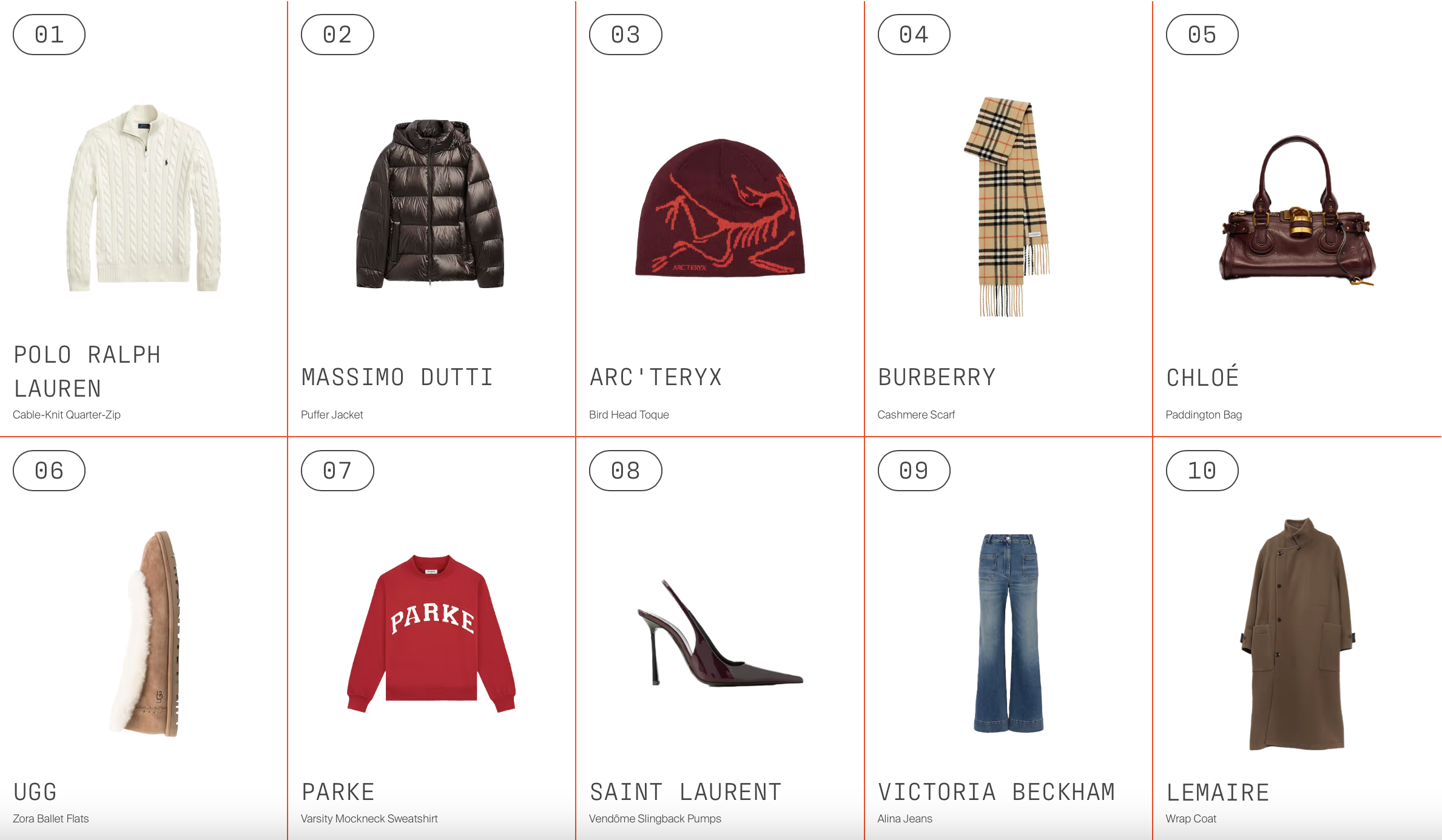

Los productos más populares del Q4 también hablan por sí solos. Los clásicos modernos se imponen -o quizás es el auge del borecore– y el lujo silencioso empieza a ceder espacio a una estética más resistente y funcional. La demanda de prendas de abrigo prácticas y accesorios sencillos refleja una mentalidad centrada en la longevidad y la utilidad. El item más buscado en el trimestre es el Cable-Knit Quarter-Zip de Polo Ralph Lauren, habiéndose disparado este tipo de prendas un 132% en los últimos tres meses. Su resurgimiento se vio amplificado por su presencia en los debuts de Jonathan Anderson en Dior y Matthieu Balay en Chanel.

The most popular products in Q4 also speak for themselves. Modern classics are taking over – or perhaps it is the rise of borecore – and understated luxury is beginning to give way to a more rugged and functional aesthetic. The demand for practical outerwear and simple accessories reflects a mindset focused on longevity and utility. The most sought-after item of the quarter is Polo Ralph Lauren’s Cable-Knit Quarter-Zip, with demand for this type of garment skyrocketing 132% in the last three months. Its resurgence was amplified by its presence in the debuts of Jonathan Anderson at Dior and Matthieu Blazy at Chanel.

Everything points to Gen Z going through a new phase of social maturity that is reflected in the way they dress: fewer logos, less noise, more classicism. Barbour, with a 147% increase in demand, reinforces this interpretation. Its growth has been driven by a year full of collaborations with names such as Ganni, Levi’s Arket and Noah NYC.

Finally, the Arc’teryx beanie has become the world’s most popular headwear accessory, with a 1058% increase in searches. Functional, recognisable and culturally legitimised.

Sigue toda la información de HIGHXTAR desde Facebook, Twitter o Instagram