Generation Z is driving the growth of shopping, and Klarna is no exception. With more orders and spending coming from those born between 1997 and 2012 than ever before, the Buy Now, Pay Later platform is positioning itself as the preferred payment option for young people.

Founded in Stockholm in 2005 by Sebastian Siemiatkowski, Klarna allows its users to pay later. There are different ways to finance online purchases: 30 days after delivery, in short-term instalments or, for more expensive items, on financing plans from 6 to 36 months.

The platform aims to offer financial control to shoppers through alternative payment options that are easy to use. It currently counts Farfetch, ASOS, Ganni, Cult Beauty and Acne Studios among its roster of fashion and beauty clients.

Klarna‘s popularity intensified with the pandemic, which fuelled the “buy now, pay later” philosophy. A more than feasible alternative for Generation Z who yearn to own exclusive products but do not have the income to live a life of luxury. And while confinement forced customers to buy online, some retailers had already embraced this type of financing before the Covid-19 crisis. Brands see instalment payments as a way to keep customers shopping even when the economy is in crisis.

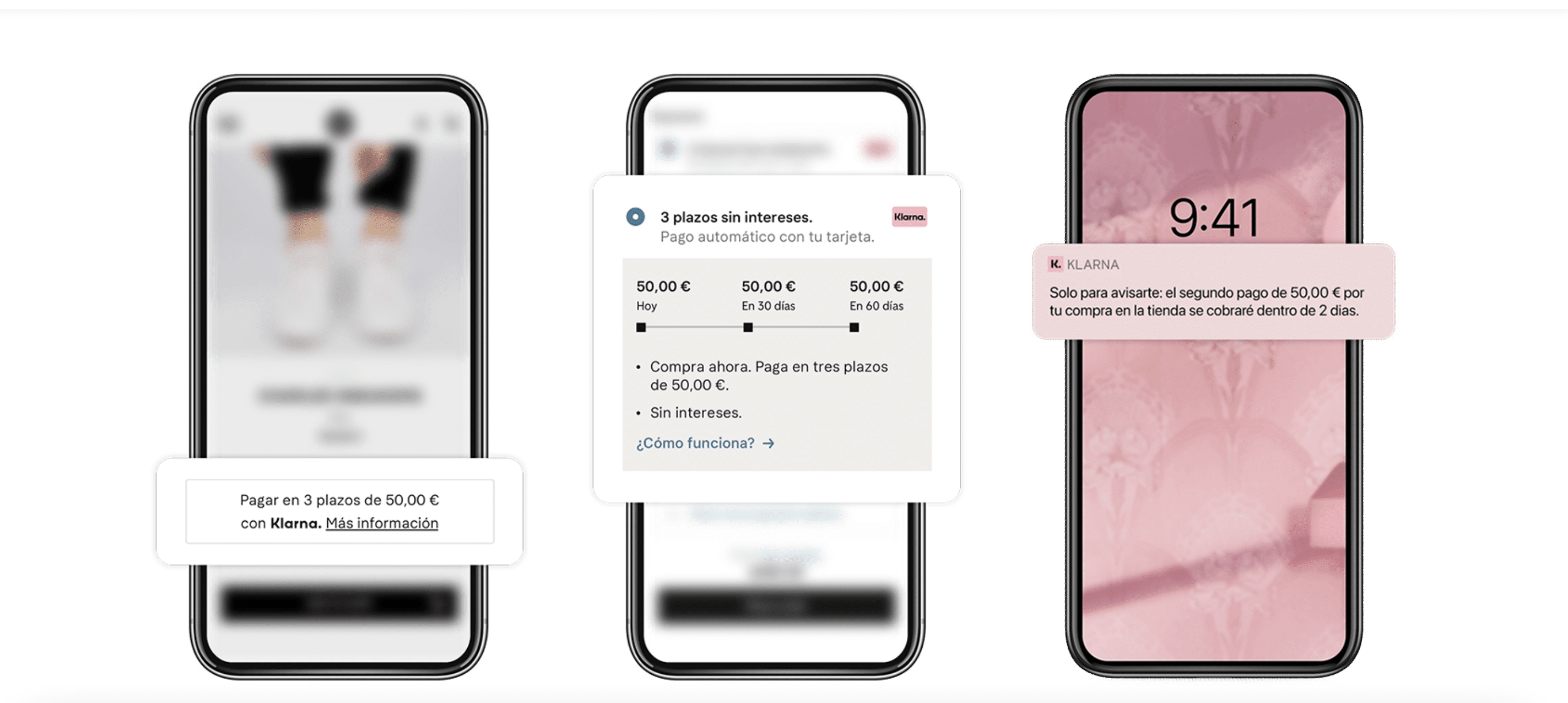

The operation is simple: You select the items you want to buy and, when you go to make the payment, you select the Klarna method. Automatically, the merchant’s website will redirect you to the official Klarna website, where you will have to enter your personal details to ensure the correct functioning of the platform and request the use of the platform. Once your application is approved, payment will be charged in 3 interest-free instalments.

Klarna‘s short-term goals include rolling out banking services in countries other than the US. Having partnered with major retailers such as Nike, Sephora and H&M, the Swedish company is looking to boost the popularity of its traditional financial offerings.

“Buy now and pay later is a commodity: it’s an easy thing to do technically. So the next thing is, why not deposit money? It’s about being at the intersection of payments, shopping and banking,” says David Sykes, director of Klarna US, “We believe that shopping, spending and banking can be interlinked in a good experience,” he adds.

What do you think of Klarna?

Sigue toda la información de HIGHXTAR desde Facebook, Twitter o Instagram

You may also like...